Putting the AI Cart Before the Power Horse

- Ishan Bhattarai

- Jan 30

- 9 min read

Data centers, the digital backbone of AI growth and development, have seen a tremendous increase in power, demand, and growth over the last year. Data centers accounted for about 2.5% of U.S. electricity use in 2015 and now consume roughly 6%, a share that is rising rapidly as AI adoption expands. By 2030, data centers are projected to draw nearly 9% of national power, with AI workloads consuming up to 40% of that total. Behind the renderings and vision decks, however, lies a critical challenge for the industry: the grid that must power this future is not yet prepared for the scale of demand being introduced. Closing that gap starts with a parcel-by-parcel understanding of where the grid can support new load and where it is already operating near its limits.

This is where LandGate shines as the operating system for AI infrastructure: LandGate connects parcels, substations, interconnection queues, and real-world constraints into a single, decision-ready view, enabling developers to effectively source the horsepower needed to enable the rapid expansion of AI.

On the graph above, the baseline load represents underlying system demand that grows steadily at approximately 3% annually. AI-driven load is added on top of this baseline and grows materially faster at approximately 17% annually, resulting in compounded total load growth of approximately 4% annually. The load forecast is based on LandGate’s extensive dataset covering data centers, AI infrastructure, offtake relationships, and future load locations, including site-control parcels. LandGate’s site control data center refers to locations where the land has been acquired by an offtaker but not publicly announced, sometimes under an anonymous LLC, and is connected by LandGate to the likely hyperscale offtaker using proprietary relationships and market intelligence.This approach provides visibility into both near-term and long-term demand growth. Generation supply shown on the graph reflects projects that are under construction, planned, proposed, or under site control, sourced from LandGate’s generation dataset, which tracks development status, location, and timing across technologies. While generation supply keeps pace with demand in the early years, it begins to lag compounded load growth in the second half of the decade. Together, LandGate’s comprehensive load and generation datasets enable forward-looking forecasts that clearly illustrate where and when supply–demand imbalances are likely to emerge.

Disconnect between load growth and electricity demand

The disconnect between load growth and electricity demand starts with how that demand has historically behaved. For decades, electricity demand increased slowly and predictably, driven mainly by population growth, economic conditions, and gradual electrification. Today’s surge in demand adds strain on regional grid operators, forcing them to scramble to keep up and often driving up electricity prices for local residents. This cadence works when demand grows in steps; it does not work when demand tries to grow in leaps.

LandGate’s national large load layer shows this shift clearly: what used to be incremental increases are now discrete, multi-hundred-megawatt blocks arriving as named projects tied to specific parcels and specific substations.

AI has turned that slope into something closer to a cliff. What began as a small, manageable increase driven by new cloud workloads has transformed into a surge unlike anything the sector has seen. Hyperscalers now talk about multi-gigawatt campuses the way they once talked about software releases, and land transactions are occurring at a velocity that would have been unthinkable even five years ago. Sites are being assembled, permitted, and power-scoped long before a final construction decision is made. This shift turns AI demand from an abstract macro story into a concrete siting pipeline you can quantify and underwrite.

LandGate’s site control dataset tracking every parcel acquired or locked up for future data center development makes this shift unmistakable.These sites appear in planning and interconnection pipelines long before the ground is broken, creating the signal of a massive wave of future electricity demand. By tracing parcels back to subsidiary entities and associated development and construction companies, LandGate can surface this demand earlier and with great confidence than traditional market indicators.

On LandGate, those “future plans” stop being vague as they become parcel geometries you can click, compare, and rank against grid headroom.

The LandGate projection shows that AI and data center load is doubling over the next five years, while generation capacity increases by only a fraction of that amount. Load growth is occurring at a multiple of planned generation additions, creating a widening gap between where demand is headed and what the grid can support. Because LandGate uniquely integrates load interconnection queues, substation capacity, and parcel-level suitability, developers can now see precisely which substations can realistically host the next wave of load and which are already far beyond their practical limits. In other words, LandGate turns the AI demand story into a siting problem you can solve: “Which parcels can deliver MW, by when, at what upgrade cost?”

Where Can the Power Come From? The Real Options to Fill the Gap

Energy Source | Speed to Deploy | Likelihood to Deliver | Key Points |

Gas Plants | Fastest bridge | Medium | Backlog through 2032+, 24/7 operation, no new turbine investment |

Renewables + Storage | Quick | High | Rapid deployment where sites & interconnection exist |

Nuclear | Medium-Long term | Low | New builds too slow for 2026–2027 gap |

Transmission / Substations | 1–5+ years | Medium | Substations limit delivery even if generation exists |

Demand Flexibility | Immediate | High | Shift AI workloads and reduce peak load |

Behind-the-Meter / Hybrid | Immediate–12 months | Medium | On-site generation but with tradeoffs |

This is the time for smart, strategic decision making. The grid can respond but the response will be portfolio-based, region-specific, and constrained by timelines.

Powering AI with Gas Plants

Supply follows a timetable grounded in physics, permitting, manufacturing, and regulatory sequence and none of it bends to ambition. New generations cannot be conjured in quarters. It must move through a years-long chain of studies, approvals, financing, interconnection queues, and construction schedules that are already stretched thin.

The unexpected return to natural gas as the stopgap of choice complicates matters further. As demand projections balloon, many utilities have turned back to gas turbines for dispatchable power that can stabilize their systems in the near term. But this strategy collides immediately with a global choke point: turbine manufacturing. Lead times have stretched, order books are packed, and the high-efficiency models required for modern standards are rolling off production lines far too slowly.. Even when utilities attempt to accelerate their pipelines, the upward slope of supply only steepens slightly. Current plants are already running 24/7, yet there has been no investment into additional gas turbine manufacturing, creating a backlog that extends through 2032 and beyond.

Another friction point is policy uncertainty. When rules shift suddenly, manufacturers and investors hesitate to expand capacity, especially for long-lead equipment like turbines. The result is a strange yet increasingly common phenomenon: plants that are financed and progressing are not waiting on permits or funding, but on physical turbines that have not yet arrived. Leaving them as power plants in architectural form, empty frames standing quietly in the landscape until the supply chain catches up.

For data center developers, this is why “announced capacity” is not the same as “available power” and why LandGate’s project-stage and timeline views matter as much as nameplate MW.

Renewables + Storage to Power AI

Renewables are being asked to accelerate inside a system that wasn’t built for speed. Solar and wind are among the fastest-to-deploy sources of new energy, and batteries are increasingly the tool that makes them firm enough to support high-value load growth.

Here’s the market logic investors care about: when demand outpaces supply, prices rise. That price pressure; whether in wholesale markets, bilateral contracts, capacity products, or structured data-center PPAs eventually improves project margins. As scarcity grows, data centers will often pay more for speed and certainty, and that overpayment can pull forward renewable buildouts especially when solar paired with batteries.

This dynamic is already visible in markets like Wyoming, where high-quality wind resources intersect with growing interest from large loads but limited near-term supply options. In these cases, wind projects that might otherwise have waited for broader system buildout can move forward sooner when anchored by committed load and firmed through storage or contract structure.

By combining this market pull with continuing improvements in turbines, inverters, and battery economics, renewables plus storage can steepen the deployment curve and meaningfully close the near-term power gap for AI infrastructure.

Nuclear to Power AI

Nuclear is re-entering the AI power conversation because it’s one of the few firm, carbon-free options, but new builds and most SMR timelines don’t solve a 2026–2027 power gap. Near-term “nuclear MW” is more realistically driven by life extensions, uprates, and selective restarts which are still valuable, but not instant.

Transmission + Substation Upgrades

Generation is only half the story; the real choke points are the wires and substations that move power to where it’s needed. Much of the US grid is over 25 years old, and many substations and feeders require upgrades just to handle existing load. Even where regional power is available, the critical question becomes: can it be delivered to this substation, to this parcel, on this timeline?

This is where LandGate’s grid reality check is decisive. By tracking substation headroom, feeder constraints, queue congestion, proposed transmission pathways, and parcel-level proximity, LandGate reveals which projects can realistically be energized quickly and which ones risk turning a 24-month plan into a 60-month surprise. It also provides visibility into how many projects are generating, injecting, or queued, giving a clear picture of grid capacity and the true limits on near-term deployment.

Demand Flexibility and “Grid-Friendly Compute”

Not every MW has to be “always-on, flat, and inflexible.” Some AI workloads can be scheduled, shifted, or curtailed (especially training runs) if incentives are designed correctly. That flexibility can unlock interconnection approvals, reduce upgrade costs, and improve project viability in constrained regions.

Behind-the-Meter / Hybrid Approaches (Speed + Control, With Tradeoffs)

In some markets, the fastest path is partial self-supply: gas engines, on-site generation, or contracted firm blocks paired with on-site storage. These approaches can shorten timelines and reduce exposure to grid bottlenecks, but they introduce fuel, emissions, permitting, and community constraints that require careful site selection.

Regulatory Shifts Don’t “Kill” Projects—They Change Timelines and Risk Pricing

Overlaying this are regulatory cross-winds, including shifting federal incentives and revised interpretations that can slow or accelerate certain pipelines. The One Big Beautiful Bill Act, signed July 4, 2025, significantly modified parts of the Inflation Reduction Act’s energy tax credit landscape, creating new restrictions/phaseouts that can translate into real project timeline changes even when demand is screaming higher. The investor takeaway is not “renewables are over.” It’s that policy volatility changes underwriting, which changes schedules.

LandGate’s solar and wind project timelines from 2020 through 2030 make these shifts visible in ways that traditional planning documents cannot. When incentives shift there is a slippage in project milestones, queue withdrawals, and revised COD dates. LandGate captures those changes at scale.

A Structural Mismatch: AI vs the Grid

Taken together, these forces create a widening gulf between what data centers hope to consume and what the grid can realistically deliver at this time. This is not an accounting quirk or a temporary imbalance that a few upgrades can smooth out. It is a structural gap—wide, growing, and deeply consequential. It will shape which regions attract AI investment, how quickly new compute capacity can come online, and what it will cost to power the next generation of models.

But structural gaps don’t just create constraints as they create price signals.When supply is tight and demand is urgent, power becomes more valuable. Tariffs in constrained zones rise, wholesale differentials widen, and capacity products and long-term contracts reflect the scarcity. And those higher prices will do what markets always do: they incentivize new supply.

This is where renewables regain momentum. Higher forward prices and a buyer base willing to pay for certainty can restore developer margins, accelerate solar + battery deployment, and attract capital back into pipelines; particularly in regions where siting and interconnection are solvable.

The LandGate Advantage: Turning the “AI Power Problem” Into a Siting and Timeline Solution

LandGate’s unified view of load projects, generator pipelines, proposed transmission lines, substation capacity, and parcel-level site control makes this mismatch visible in real time. Developers using LandGate can see not only where “planned” power is likely to materialize or stall in the queue, but also when data center projects are proposed, approved, or are expected to be completed. This visibility reveals where AI demand will collide with physical limits such as substation headroom or transmission bottlenecks long before peak loads arrive. This is the new playbook: win the land race by winning the grid reality check first.

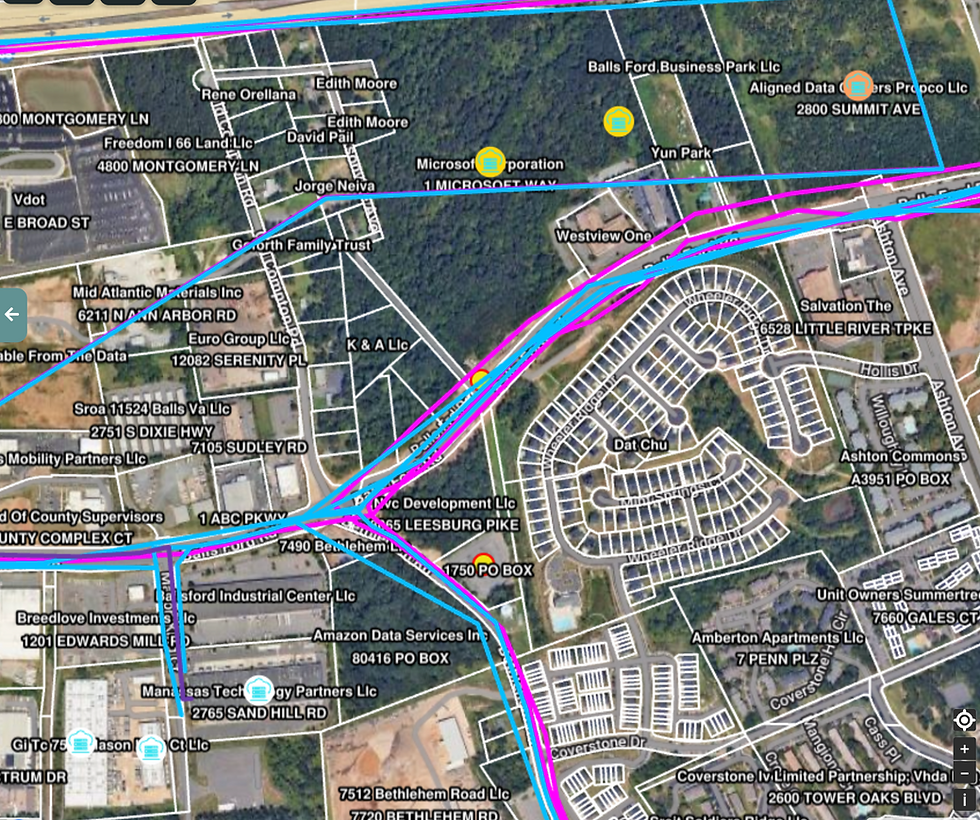

It is already influencing land values, transmission planning, siting decisions, and the behavior of developers who are beginning to understand that securing electrons is now just as important as securing real estate. In markets like Loudoun County, VA where LandGate’s infrastructure data shows substations with effectively zero remaining capacity; the constraints shaping the next decade of AI growth are not hypothetical. They are mapped, measured, and already altering development patterns. LandGate doesn’t just show that constraints exist but also shows exactly where they are, what feeds them, and which nearby parcels still have a credible path to power.

This is the reality we are entering: an AI cart accelerating at full speed while the power infrastructure works to keep pace. The next five years will determine whether we bring these trajectories into alignment, turning rapid AI growth into a coordinated expansion rather than a bottleneck. No matter how advanced our models become, how many trillions of parameters they hold, or how fast hardware improves, none of it matters without the electricity to make it run and electricity cannot be scaled overnight. For those citing AI infrastructure, the competitive edge is no longer just capital or construction speed; it is the ability to identify parcels where power is reliably deliverable. That is precisely where LandGate provides clarity and confidence.

To learn more about the pioneering tools & data available to data center and load project developers, book a demo with our dedicated infrastructure team.